Based on my anecdotal experience this seems to very much understate inflation.

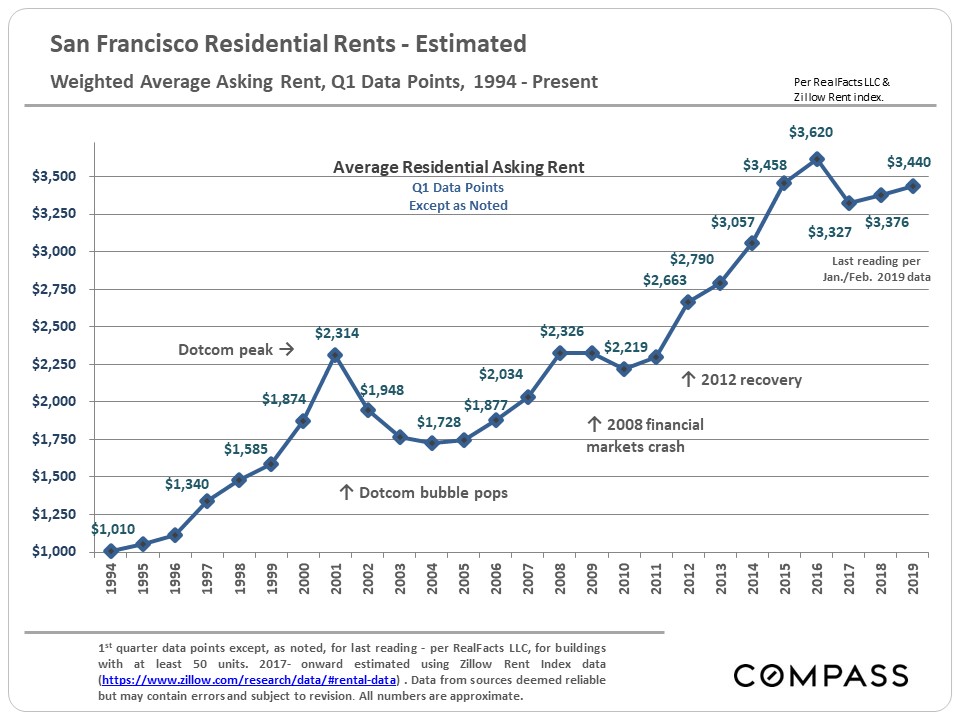

How is housing up only 3.8%? This site says over 17% rent increase nationally over the last year: https://www.apartmentlist.com/research/national-rent-data which seems to be more accurate. Anyone with a web browser knows that home prices have experienced a monumental increase.

Also a trip to the grocery store appears to cost me 50% more now for essentially the same goods. Every trip to the store pre-covid cost me around $100, now its $150. I do buy primarily proteins so that is the source of the increase but to ignore that seems ill advised.

Not generally a conspiracy theorist but unless the people that built this report are using some accepted formula that is very different than the real world this report seems to be intentionally underselling inflation.

The BLS has a very well-documented method [1] of measuring core consumer inflation. The basket of goods they track likely does not reflect your personal consumption patterns.

Core inflation excludes food and energy. So as long as you're dead, you only experience core inflation! Everyone else who is alive is exposed to core inflation and also the one that takes food and fuel into account. Perhaps that's why people don't "buy" the numbers. Because the numbers aren't representative of the reality that alive human beings experience.

Core Inflation is needed so that they can apply the right monetary policy. If you want your 'personal' inflation, they have data for that too.

Fed releases all kinds of data (unemployment and monetary) and is pretty transparent.

It is disingenuous of you (and contributing to the erosion of institutional trust of Federal institution) by falsely accusing them.

Federal agencies aren't perfect, but at least educated people in HN should take the responsibility of giving constructive criticism based on facts rather than being brainwashed by random YouTuber/Blogger who is generally clueless about economics

Still waking up and it's possible I misread GP, but their comments didn't seem disingenuous on my reading. It's healthy to be skeptical of something that varies that much from one's personal experience. Your reply about data available for personal inflation was exactly the kind of information they needed to verify if the underlying data matches their personal experience.

I understand the sensitivity to folks spouting "fake news", but let's not discourage critical thinking in a time where there is precious little to go around.

It's NOT healthy to assume you're the 'average' when you are not.

Almost no one on HN is reflective of the 'average' American and that lack of understanding is part of the reason the poor suffer so much in policy decisioning.

I don't know enough to comment on "healthiness" of assumptions about ones' self and where they fit into analysis like in the OP's link. My commentary is purely on how we communicate with each other in a time where divisiveness, misinformation, and polarization are common and pervasive.

It's hard, but if we want to have productive discussions we need to treat each other with empathy and talk to the best possible interpretation of each other's arguments. This assumes people are coming to a dialog in good faith, but everything needs to start with a little trust somewhere. Trolls are also not too hard to spot.

The median salary for software developers in 2019 in the US was $107,000, with 50% between $82,000 and $136,000. The mean salary in California was $134,000 and the mean in San Francisco was $145,000. (https://money.usnews.com/careers/best-jobs/software-develope...)

The median household income in the US in 2019 was $69,560 with a 90% confidence interval of <$1000. The "median earnings of all workers aged 15 and over with earnings" in 2019 was $42,065. (FWIW, the median household income for black people in 2020 was $46,000, and for Asian people was $95,000.) The median household income of those with no college education was $47,000, some college was $64,000, and at least a bachelors degree was $107,000. (https://www.census.gov/library/publications/2021/demo/p60-27...)

(The median household income in California in 2019 was $78,000.)

The median salary for software developers individually in 2019 therefore puts them in the highest 40% of households. (In 2019, 1/5th of households made less than $28,000, 2/5 made less than $54,000, 3/5 made less than $86,000, and 4/5 made less than $143,000. 95% made less than $270,000.)

For many of the people frequenting HN, this is your mileage in the act of varying.

If you want productive discussions that you need to enter them in a good faith.

Building an argument based on personal anecdotes and applying it to national policy not good faith. Science literally exists to limit subjective bias and to separate actual trends in reality from notions in your head, subjective experience basically worthless for understanding large-scale trends.

It's always alarming to me to see how many people on HN don't acknowledge the bubble they're in.

If you're a well-paid engineer, and nearly everyone you interact with is a well-paid engineer, you're going to think everyone lives like you.

And I wonder how many of them grew up poor. And I mean, poor as in "half my meals as a kid were rice and beans", not "One time my dad didn't get the bonus he was expecting, so we had to fly coach rather than First Class when we to France during Christmas".

Questioning the BLS data without being able to explain how the data is collected and analyzed is not a way to fight misinformation, it's a way to encourage it.

If OP had made some more detailed arguments, like 'the methods for imputing homeowners rent seem biased' or 'it seems disingenuous to keep a static weighting during COVID, despite the major observed shift away from services and to goods' then I would love to engage on that.

But randomly saying 'this EXTREMELY transparent dataset seems fishy' is just encouraging people to 'do their own research' on things they have no expertise in.

"In 1996, five economists, known as the Boskin Commission, were tasked with saving the government $1 trillion. They observed that if the CPI were lowered by 1.1 percent, then a $1 trillion could indeed be saved over the coming decade. So what did they do? They proposed a way to alter the formula that would lower the CPI by exactly that amount!

This raises a question: Is economics being used as science or as after-the-fact justification, much like economic statistics were manipulated in the Soviet Union? More importantly, is anyone paying attention? Are we willing to give government agents a free hand to keep changing this all-important formula whenever it suits their political needs, simply because they think we won’t get the math?"

This was written by Edward Frenkel, a math professor at UC Berkeley who was born in the USSR in 1968 and so, we can assume, had some familiarity with statistical games played by regimes trying to hold onto power.

I invite you consider that you might extend too much faith toward federal institutions that have presided over a ceaseless rise in inequality and erosion of rights in recent decades.

And he is not an economist, yet he is a well known econ crank.

Here's an actual economist [1], looking at the evidence one decade past the Boskin report - concludes the same thing.

And, the really cool thing about inflation over that length of time, is you can check it for yourself (which I have showing people why ShadowStats is complete nonsense).

Get some old ads from the start of the period (say 1996, the year of the Boskin Report), and look at prices. Put them in excel. Do the same for now. Compute a reasonable basket.

And here is the really neat part - see if the BLS reported CPI over that period matches reality, or if adding 1.1% annually matches reality.

I will spoil the result - BLS is correct.

From the CPI calculator, Jan 1996 to Jan 2021, inflation is a 1.69 multiplier, for an annual rate of 2.12%. Add back the supposed 1.1%, take the 3.22% over the same 25 years, get a 2.21 multiplier, quite a difference.

And, for the record, there are lots of other places tracing inflation, like the Billion Prices Project, that reach the same conclusions. If the govt lied about it, there would be awesome arbitrage opportunity (and like all such things, people have even investigated that - no such lies - papers on Arxiv).

Google any inflation linked asset, from bonds, ETFs, swaps, all sorts of derivatives. If you know inflation is consistently wrong, all such things are mispriced. Then it's simple to hedge against non inflation versions of the same, or buy derivatives constructed against them, to extract the risk free difference.

If you dig around you'll find finance papers measuring such things, demonstrating no one has found any such exploitable gaps. Plenty of groups try.

>In 1996, five economists, known as the Boskin Commission, were tasked with saving the government $1 trillion. They observed that if the CPI were lowered by 1.1 percent, then a $1 trillion could indeed be saved over the coming decade. So what did they do? They proposed a way to alter the formula that would lower the CPI by exactly that amount!

I know this is a direct quote from a Slate article, but it's a blatant lie. The commission was officially the "Advisory Commission to Study the Consumer Price Index", i.e. it's founding purpose was to evaluate the accuracy of the CPI, not an open-ended mission to save the government money.

This is why cryptocurrency was invented. Satoshi even signed a statement about government bailouts in the first bitcoin transaction.

The truth is that the game is rigged. Like entropy, government power always increases over a long enough timeframe. Anytime the spotlight is shined on government they manipulate the game or blame corporations. Then they introduce regulation to "protect" citizens but these regulations add up to just keeping big business entrenched.

Satoshi doesn't get any credit for stating what people have been stating literally for decades before "he" came along. Let's not give him credit for anything other than the bitcoin algorithm.

> It is disingenuous of you (and contributing to the erosion of institutional trust of Federal institution) by falsely accusing them.

There are trillions of dollars tied to these inflation numbers. Many social services are tied to these values. So if an agency could get reported inflation down just a few basis points based on their subjective decisions on what to include and what to substitute, that could save the government billions.

That's not saying that they are necessarily doing that, but its wise to be suspicious when there are such large stakes

That suspicion should motivate people to educate themselves before pushing conspiracies. Public debate needs a core set of facts to reason about the world so politicizing BLS numbers is... really bad.

That suspicion should motivate people to think about the incentives they're setting for government agencies and try to create clear objective measures that cannot be gamed.

> Public debate needs a core set of facts to reason about the world so politicizing BLS numbers is... really bad

When it becomes tied to trillions and the agencies are selected by politicians then its by definition political.

> create clear objective measures that cannot be gamed

There is no perfect world where nothing can be gamed. We have a respected institution in the BLS and setting an impossible bar only promotes misinformation by discrediting what's credible.

> the agencies are selected by politicians

This is why there are specific roles for political appointees and others for career civil servants.

In this specific case, we're talking about the usual noise of someone not understanding the point of core inflation, not knowing that there are other measures of inflation, and jumping to a conclusion that the numbers must be bogus. Regardless of what you think about inflation numbers, the reasoning was bad.

None of us posting here has any responsibility to upholding the trust of federal institutions, which have already been eroded far more than one could do on HN by both parties to hold power.

Really? They don't want to track the inflation that results from the new money just being buried in stocks and real estate for safekeeping? Isn't that an indicator they're printing too much?

I don’t drive, I’m mostly on a plant-based diet, and I’ve been on 100% renewable energy for years. I’m very much alive, and also am willing to believe we’re not close to double digit inflation based on my costs.

And I live in one of those high-priced metros, so I actually experienced a rent cut since everyone fled to Miami and Austin (thereby increasing prices there).

Obviously your experience may be different, but remember econometrics tracks the entire economy, not just your budget.

“ experienced a rent cut since everyone fled to Miami and Austin ”

Obviously not in a California metro where the state decided to subsidize rents to compensate for preventing evictions resulting in a windfall for landlords and massive rent increases throughout the state.

That's the thing, there is no one "average" American that this inflation number applies to! It aggregates over all of them, including the ones living on plant-based diets and using 100% renewable energy

The average american has 1 breast and 1 testicle. The term "Average American" tend to be used by people claiming to talk on behalf of them, without actually doing so (given that the "Average American" is as different from the "Average American" as everyone else)

The consumer price index does include food and energy. It's in the main table of the post we are discussing. It's not clear why you are not 'buying' them.

What we need is tools that help individuals plug in their budget and track how inflation affects them. These overall inflation figures are pretty much useless because they have to exclude information in order to not be too highly amplified in either direction. Creating a budget of how much I typically spend on food, gas, utilities, and such and being able to backtest that budget would be really helpful, and perhaps that data could be used to crowdsource inflation figures that are more representative of what the average person is actually experiencing.

Inflation is not the same thing as cost of living. Inflation measures changes in the price level, while cost of living is the expenditure that is needed to sustain a particular standard of living.

* factoring in technology as deflationary. yea, your phone is 20% more expensive, but it has twice the computation power, so it's actually a deflationary component

makes sense, considering that most people own their homes, aren't exposed to the housing market, and aren't buying houses every month.

>* factoring in technology as deflationary. yea, your phone is 20% more expensive, but it has twice the computation power, so it's actually a deflationary component

Why do you have to get the flagship phone? Why not get a low end phone today, that has about the same capabilities/speed as the phone you had 5 years ago?

It's not about WHY you "have to" get a flagship phone. It's about the fact that the flagship phone is 20% more expensive than it was 5 years ago, yet that isn't counting toward inflation with the CPI. Christ, we could use a standard of computation from a 1980's calculator and REALLY offset rising food prices. Hence the gamesmanship. Maybe I can offset the rising cost of my food basket by switching out to lower quality (or shrunken) goods for the same money, but you can't look me in the eye and tell me I have the exact same buying power as before with the same money.

The point is that if you want a phone with the capabilities and performance of a good one from five years ago, you can buy that today. It will cost you substantially less (in nominal dollars) today than it would've cost five years ago. How does that not represent a person with a given number of dollars being able to buy more, in this instance?

“ factoring in technology as deflationary. yea, your phone is 20% more expensive, but it has twice the computation power, so it's actually a deflationary component”

I guess you could also make increases in health care costs go away with this approach. It’s way more expensive than 20 years ago but the tech is way better so it’s actually cheaper.

I'm not sure where you're getting "technology is deflationary" since I basically need 1 phone at least, doubling it's speed doesn't really give me any more utility for the most part as I, and most people, don't really get any added benefit out of that. It also doesn't let me get by with half a phone, since a half phone is useless.

Given how much is at stake when it comes to government spending and the economy at large, I highly suspect CPI has been a victim of Goodhart's Law for quite some time.

Its not about the documentation, its about the complexity and subjectivity (e.g. substitute goods, weighting of regions, remove outliers, and quality adjustments). I'd much prefer a simpler "less accurate" measure like the change of a fixed basket of goods from two periods within a short time period and an updated basket to be used for the next period. That way you're not stuck w/ buggy whips on your CPI index. Instead we have an indiscernible mess that doesn't reflect reality and that no one trusts.

The basket of goods it tracks may not reflect popular consumption patterns and it’s possible the measurement severely minimizes the inflation most people observe.

If that's the case and I tend to agree that it is, then it should essentially render this report useless as a means of gauging how the economy is affecting most people and should be rebuilt with very different measurements.

They update CPI regularly to reflect what people are currently buying. The economists and professionals who work in this industry aren't idiots.

The CPI index has been running continuously for decades and yet you've decided based on one uninformed HN comment that we need to scrap it and rebuild it with different measurements? Peak hubris.

I spent ten years building and maintaining one of the most important economics time-series databases in the world (tracking the US chain store sales index), if that's a credential.

You can search around for plenty of criticism of the CPI if you're interested. The former is reviewed by a guy with a doctorate in economics from Harvard. Is he "uninformed"?

This is all fair and there are hundreds of economists who will admit that CPI has plenty of shortcomings - I don't think anyone would say that it's perfect or even hugely accurate. However the value of CPI comes from the fact that it's the accepted "compromise" for weighting and measuring inflation across the largest economy in the world.

If you believe that CPI isn't accurate and your methods more accurately represent real-world inflation conditions, there's a ton of money to be made betting on the TIPS spread.

> The basket of goods they track likely does not reflect your personal consumption patterns.

Or anyone's, really.

It's not really consistent either, because hedonic adjustments are effectively "arbitrary". BUT at least they are published, so you can, if you had the time, look at all of the fudge factors they drop in and decide for yourself how much skepticism to apply.

You're noticing what's gone up. I just did a Home Depot run and everything there was the same price it was last year.

A 7% inflation rate is not everything going up 7%, it's a small number of things going up a lot. The human mind is a lot better at noticing things that change rather than things that don't, so inflation always seems larger than it is.

Inflation is worse depending on your region. If you live in a coastal state, you are experiencing less inflation than if you live in the flyover states.

The observation actually strikes me as the ground truth. Inflation feels trivial on the coasts and brutal in the interior.

But I don't buy the explanation.

I think a better explanation is that the midwest and south have benefited from being in an incredibly low-friction trading bloc with a few extraordinarily productive states, while not having to compete for resources (land, goods, or services).

A variety of forces have caused that trading bloc's productivity to more uniformly distribute.

It's easy to sit in MO and say that we need "more Main Street less Wall Street". Until a hundred phd-holding 40+ year olds who've been making mid six figures and barely affording rent on 600 sqft shoeboxes for the last decade show up in on Main St and are willing to best any offer on their preferred houses. In cash. Suddenly "spreading the riches" sounds more like "oh shit I have to compete with all this wealth and education that used to be concentrated in midtown manhattan/SFBA".

Turns out that the massive rent/service disparity in the USA was unsustainable. But, instead of prices "normalizing" on the coasts, the middle won't stay cheap. Not sure there's any good solution to that, other than the midwest and south becoming more productive and better educated.

This round of Inflation is just the midwest's snow white main street realizing what gentrification means.

So the bulk numbers say it's up apparently, I'm getting roofing quotes currently and roofers say it's back down to pre-pandemic levels, at least where I am. There are a lot of different wood products out there I guess.

I'm not sure if this is the case with these data sets, but one common difference that causes confusion are current advertised rates vs total inventory. It could both be true that apartments on the market cost 17% more, but all rents (including those not marketed or not renewing) are only up 3.8.

Another methodological difference might be mix of goods. For example, you probably can afford to pay 150/grocery-visit, but someone else might have just cut their meat intake, or switch to cheaper cuts, or have otherwise substituted such that maybe they pay $120. If you measure by the visit, or gross store receipts then the numbers will seem lower than they would comparing the same exact goods.

It's because they measure the item to an equivalent item from 1970. Take a car for example. Modern cars have various electronic contraptions that didn't exist in cars in 1970. A car today will have electronic control of windows, rather than the mechanical control from 1970. So, the BLS considers inflation by replacing a modern car's electronic control of windows and replaces it with what you can buy with a mechanical window today. It does this for all parts of the modern car to make it an equivalent product of 1970. Only when all parts are equal, they will calculate inflation.

Yes, I thought that CPI series were bullshit and to prove it I decided to start looking at ads in newspapers from many decades in the past. I thought that while technology has advanced, some things are the same as we've always had so I could just compare real advertised prices over the years.

Turns out that is not the case. Somehow a quality men's overcoat used be comperable in cost to a piece of land on the west coast that is now worth tens of millions of dollars ( and has been for decades now) When you consider where that coat came from then and what it took to get it to where it was offered vs what the practical value of that land was at that location and time... trying to compare prices of things over 50 years is like trying to compare the minutia of two different worlds you don't understand. It's impossible to cleanly bucket like for like over time when the price depends so much on "this level of thing, at this place and at this time" just as it's impossible to centrally replace the "invisible hand" in setting prices now. It's super complex to reverse engineer in hindsight why the relative prices of things were as they were at some point in the past.

Not saying that government stats don't cheat. I think they do because they have motive to do so. But I fully agree that the task of creating a useful price index over a long period of time, even a short few decades, is far from a simple problem. Anyone who doesn't agree: please go try to make one.

You should look into how they calculate the numbers haha, it’s comical. They send letters to homeowners and ask them “How much do you think you could rent your house for?”

There’s no need for this idiocy I’m sure one of you could scrape the Zillow website in an afternoon and come up with something better.

You are confusing "rent" and "imputed rent". The former is easy to calculate, and the BLM does calculate it accurately by simply asking a whole bunch of renters how much they pay each month.

But imputed rent is a more subtle and difficult number. The goal is to know what the market rent would be for all the homes not currently on the rental market. I'm sure you can find other sources on why this value should be included in the CPI calculation (in addition to rent), but once you recognize that, it should be clearer why the Zillow approach wouldn't work: Zillow and similar sites only know about what homes sell for, or rent for.

Now could an expert come up with a model of what a home might rent for given sale price, number of sqft, bedrooms, etc.? Of course. But doing so very much isn't an afternoon project because the data is tricky: the owner occupied homes differ from rental units in important and hard to evaluate measure. For instance, apartments around my city are more poorly maintained than similarly aged ownership units.

>The goal is to know what the market rent would be for all the homes not currently on the rental market

I don't understand why this is necessary, or why asking someone who hasn't been on the housing market for 15 years what the value of their home is might be good data collection.

I'll let someone else comment on the data collection part. But for why this is necessary, how else would you compute the housing costs of someone who purchased a home 15 years ago and hasn't moved since? That number is needed to compute the overall CPI, so you can't just skip it

Why can't you just skip it and calculate a median of all the nearby homes and rentals that have transacted on the market over the past x months? That seems more objective than asking people who have no idea what rent is what they'd rent their home for.

I bet if you asked a panel of 1000 homeowners that haven't bought or rented in 10+ years what rent was going for in their cities, they'd undershoot it by 20% or more.

To quote the BLS [0] on why home prices are the wrong metric:

> the CPI views housing units as capital (or investment) goods and not as consumption items. Spending to purchase and improve houses and other housing units is investment and not consumption. Shelter, the service the housing units provide, is the relevant consumption item for the CPI. The cost of shelter for renter-occupied housing is rent. For an owner-occupied unit, the cost of shelter is the implicit rent that owner occupants would have to pay if they were renting their homes.

If I'm reading that fact sheet correctly, they actually don't ask homeowners at all. Rather they just ask a bunch of renters whet their monthly rent is (which the vast majority of them should be able to answer accurately) and then use fancy math to extrapolate what the nearby home ownership units would rent for.

I'd suggest reading/skimming that whole fact sheet if you want more details, though the summary seems to be that they've actually put a bunch of thought into this stuff.

sure but they could easily scrape Zillow in 2020 and compare the numbers to 2021. Those numbers would show a ~17% increase. If they are unable to adapt their model to modern data sets then the model is pretty much useless.

Edit: General response to the responses. I am not advocating for Zillow to be a source of truth, I was responding to the parent comment of my post and their mention of Zillow. What I am saying is that we are not limited to using methodologies of the past, there are vast datasets and modern data collection methods available to us now that can be used.

Considering the financial issues Zillow is experiencing, I'm not sure that it makes sense to trust their pricing models. Zillow and Opendoor bouncing off of each other has given some neighborhoods the real estate equivalent of Amazon's book about flies that was algorithmically priced at $24 million (https://www.wired.com/2011/04/amazon-flies-24-million/)

Zillow's model is fine in the aggregate, which is what the parent was suggesting it for. They ran into trouble profiting from it because adverse selection hits them hard -- they'll only be able to buy from the very homeowners whom the model most overpredicts the value of, because of unobservables it can't model.

None of that relates the question of whether Zillow, on overage, correctly predicts how much the market, in the aggregate, has moved.

I think you're confusing separate issues because they both merge into a narrative of "zillow bad".

> I'm not sure that it makes sense to trust their pricing models.

Zillow, Redfin, etc list at prices that may be inflated, but they always list the purchased pricing as far back as they can and raise estimate to last sale if higher.

I live in Berlin Germany. I've been manually tracking all my grocery costs over 2 years now in an Google Spreadsheet. I'm a single person and I buy organic food. I work from home and I don't eat a lot outside. I cook probably on average 1.5 times a day. My general monthly bill on food is 600€. My methodology has been this:

- I pay all my groceries with my debit card

- Then, to get the cost for a month; I take all debit card entries in my online banking and sum them up

- I then compare the finding to older findings.

Last time I checked, the costs of my groceries hasn't gone up. So far, it has never gone up in any significant form over the last two years. Maybe by 5% but by no means +50% like the parent post suggests.

I sometimes also get anxious about "inflation" when the cashier quotes an unexpected price. And it's why I've started double checking my intuition with the above-outlined process.

Indeed, some times the shopping ends up more expensive as e.g. I bought an extra pack of coffee or meat.

Humans aren't robots folks, if there's consistently some excess food being disposed of it could simply mean there's slightly less going into the wastebin.

And regarding TP, I don't know about you, but I tend to be wasteful with TP when the roll is fresh and increasingly frugal as the roll approaches empty.

This is all highly subjective but the fact is people tend to be inconsistent and wasteful.

You need to track normalized unit costs for such data to be reliable. Package sizes are constantly being manipulated, period.

Wouldn't it though? I mean, caloric intake doesn't fluctuate much. If smaller sizes were ending up leaving this person hungry, presumably they'd end up buying more to compensate.

Not generally. Vast majority of people eat well past simple hunger satiation. In regards to non edible goods, a few less sheets per paper towel role would likely not be noticed in the short term but taken over a year would like reflect an extra role or 2 purchased.

You would also need to consider if you changed any purchase habits. If you comparison shop, or focus on buying whatever cut of meat is on sale, or similar, then you might actually be buying a different distribution of items.

Like OP said, they live in an expensive West European city and buy almost only organic products which consists, in part, of meat and imported products.

I myself live in a West European cit and buy almost only organic products that are plant based and mostly locals. It costs me around ~300€/month.

Still, OP pays double that. But :

- The city I live in is way smaller than Berlin so it's obviously cheaper (going often in Paris for work, I can assume by how much)

- I don't eat meat. Organic meat is probably (after luxury restaurant) the most expensive way to feed someone so I have no doubt that if I added meat to my diet I would be paying (a lot) more than 300€/month

- 80% of my vegetables come from a local farmer with whom I have a yearly contract, which divide probably by two the vegetables cost compared to buying them in a store

- Except for a few things that can't be cultivated locally (at a country scale), most of the food I buy didn't to make more than 1000km to arrive in the shop

- I'll take a wild guess but while 80% of what I buy is "raw food", OP is probably buying more prepared product which again makes it more expensive

- Another guess but OP is probably making their groceries in a in-town shop where prices are higher (because of rent and delivery constraints) than shops around town made for suburban people, while in my case I go in those cheaper shops to take advantage of the longer route to ride my bicycle more

All that combined, I'm not surprised by the figures given by OP since they're eating one of the most expensive diet a Western European can eat. And I'm not saying it in a bad way. I'm just trying to see facts.

That's not at all crazy. Spending 600 euros or dollars monthly on food for a single person is actually quite reasonable—as another commenter pointed out, it's about 20 euros per day for all three meals.

In my experience, "moderately expensive" restaurants (I don't actually go to what I'd term "very expensive" restaurants) come in at $40-50 per plate. That means that just for dinner, if they were going to very expensive restaurants every day they'd be paying roughly twice what they quoted.

They said they were talking about "grocery costs", and later clarified it was groceries only [1], which is very different from restaurant prices.

For comparison, our household (US) spends ~$200/person/month on groceries (also with very little eating out). Food here in the US is cheaper, and we aren't mostly buying organic, but we are using Instacart. I'm also surprised they are getting such a large number.

I don't really see anything crazy about this. Poster eats organic food and lives in an expensive city. If he works out he probably consumes a good amount of food.

I know the prices in Germany. I can see how one would spend €300 or even €400... but €600 just seems a lot. Maybe if you eat a lot of expensive imported items and such.

"Anyone with a web browser knows that home prices have experienced a monumental increase."

An asset cannot experience inflation. The word inflation suggests something that loses values. A home that gains in value is clearly not suffering inflation, rather, that is the opposite of inflation.

If you earn $200k a year, and there is 5% consumer inflation, and a year later you still make $200k, then in a sense you are 5% poorer.

If you've a house worth 200k and its value goes up 5%, then a year later you are 5% wealthier.

We might joking and informally refer to "asset inflation" but please remember, under any formal model, there is no such thing; it would be a contradiction in terms.

Are you really 5% richer, if realizing that appreciation means selling the house, and buying a comparable one on the market that has also appreciated 5% in value? Plus, depending on your locality, your property taxes went up due to the new valuation. The only way you're unlocking that value is if you sell the appreciated asset for some good/service that hasn't gone up in value, say, televisions. Otherwise, you're just trading it for other expensive goods and your purchasing power hasn't changed.

I'd argue even if absolutely all housing went up 5% in value, everyone is still at least a little richer (albeit not effectively 5% richer and mostly on paper still).

Most people buy a house with a down payment. A conventional down payment is 20%. If you bought a house for $100,000 (with $20k down) and it's now worth $105,000. You can now sell the house, and put $25k down on another house, which means you can now qualify for a $125,000 house. For simplicity I'm ignoring principal that had been paid down on the first mortgage and transactional costs.

Those are all valid concerns, but unrelated to the conceptual issue of whether an increase in the nominal price of an asset can be coherently understood to be a form of "inflation."

>If you've a house worth 200k and its value goes up 5%, then a year later you are 5% wealthier.

That doesn't follow. A nominal rise of 5% doesn't make you 5% wealthier. Asset PRICE inflation is a real thing. You're conflating value appreciation and depreciation (rise or fall in real value) with price inflation/deflation (rise or fall of nominal value).

Houses are not consumer goods, they are assets, like stocks on the stock market. If the stock market goes up 2%, we do not make a habit of saying "Terrible news today, the stock market suffered 2% inflation."

This sentence is unmanageable:

"You're conflating appreciation and depreciation (rise or fall in real value) with inflation/deflation (rise or fall of nominal value)."

First of all, I'm explaining the government's definition of consumer inflation, which you seem to misunderstand. The government does not formally model rising asset prices as consumer inflation, the government models that increasing wealth.

Second of all, you're conflating nominal appreciation and nominal depreciation with the concept of the "real," which is to say, inflation adjusted value. If the value of your house increases by 5% then you are 5% wealthier. Whether this has kept up with the pace of inflation is a separate issue. We need to talk cleanly and cogently about nominal value versus real changes in value. You can do that by adjusting your changing value of wealth by the consumer inflation, but clearly you cannot do that mental adjustment if you're trying to base the calculation off the real value of your assets -- in that case you would be double counting the inflation.

To put that differently:

Suppose your house increases a nominal 5% and consumer inflation is 6%. You might say "Oh, I'm 1% poorer in real terms." But you can't say that if, as you seem to want, asset values are included in the calculation of consumer inflation. In other words, if the 5% increase is already part of the 6% increase, then you've mushed the concepts together to such an extent that the calculation becomes meaningless.

>Suppose your house increases a nominal 5% and consumer inflation is 6%. You might say "Oh, I'm 1% poorer in real terms." But you can't say that if, as you seem to want, asset values are included in the calculation of consumer inflation. In other words, if the 5% increase is already part of the 6% increase, then you've mushed the concepts together to such an extent that the calculation becomes meaningless.

You've mushed them together, not I. We were talking about asset price inflation, and then you tried to mush it together with consumer inflation.

On the whole you are right and no disagreement from me. The measure of inflation uses shelter though so rising home purchase prices generally means that when those same house purchased at a higher price are rented out the price they rent for is likely going to be higher, raising costs for non owners. So yes, you are correct but rising home prices while a good thing for the owners that got in before the prices rose is not a good thing for anyone else. With that said I am a home owner that is happy my house has increased in value but at the same time, it generally means nothing to me as if I wanted to move I would have to buy another house that has increased in value as well. Its only positive return for me is if I take out a loan on the house it allows me a lower LTV and subsequently a lower interest rate on that loan.

Absolutely true, and I was in no way suggesting that rising prices for homes was good or bad. I've tried to stay neutral on that issue. The point, which is important to this conversation, is that nominal increases in the price of an asset cannot coherently or conceptually be understood as a form of "inflation."

The phrase "asset inflation" is one that we can use jokingly and informally, but formally it would not make any sense in any real attempt to judge changes in the standard of living.

By contrast, these are all valid questions:

Are wages going up faster than the nominal price of homes?

Is labor productivity going up faster than the nominal price of homes?

Is the share of national income going to labor increasing or decreasing?

Is asset wealth increasingly held in liquid or illiquid forms?

Is average rent going up faster than average wages?

Your nominal profit is 5% and your real profit is 0%, good point, but unrelated to the conceptual issue of whether an increase in the nominal price of an asset can be coherently understood to be a form of "inflation."

But housing costs money. If you're a homeowner, if you bought a house for $250k in 2019 vs. a homeowner who bought an identical house for $300k in 2021, its pretty hard to argue the second homeowner isn't comparatively worse off.

Of course, houses have to be maintained. At least where I am, the cost of plumbers, electricians, HVAC, etc. have exploded in the last 18 months.

Renters are a much more straightforward case. The costs of housing (i.e. the costs of purchasing and maintaining the asset) are passed on to them in the form of rent increases.

While your concerns are valid, that is simply not the definition of consumer inflation. Houses are not consumer goods, they are assets, like stocks on the stock market. If the stock market goes up 2%, we do not make a habit of saying "Terrible news today, the stock market suffered 2% inflation."

>we do not make a habit of saying "Terrible news today, the stock market suffered 2% inflation."

If the real value of the underlying equities/assets of the market stay the same but the nominal price goes up 2%: As a cash buyer I would absolutely say "terrible news today, the stock market suffered 2% price inflation today."

Just because the government doesn't put that into the "consumer inflation" figures doesn't mean it doesn't look like inflation to me as someone who may desire to own certain equities.

The word "real" has no meaning in this sentence unless you've first developed a concept of consumer inflation that is separate from asset values increasing. If you say that asset "inflation" should be a component of the consumer inflation that the government measures, and therefore consumer inflation includes the increase in the value of homes, then the word "real" has no meaning. You cannot say "Houses went up 5% but inflation also went up 5%" if the 5% increase in homes is already counted in the 5% inflation. You are mushing these concepts together and creating a conceptual mess.

>If you say that asset [price] "inflation" should be a component of the consumer inflation

First of all I never said that, because by definition they are two separate things.

Asset price inflation refers to a fixed quantity of currency buying less and less real assets. Consumer inflation refers to a fixed quantity of currency buying less and less of the basket of consumer goods and services.

You keep confusing yourself by sometimes mushing the concepts inflation, asset price inflation, and consumer inflation and then getting upset when one doesn't fit neatly into the other. You are mushing these concepts together and creating a conceptual mess.

You can play this disingenuous game all day where you mix the 3 concepts around, and yet at the end of the day asset price inflation will still be real.

What is a real asset? If by "real" you mean "adjusted for inflation" then, again, you are double counting the inflation. If by "real" you mean "an object with a clear category and a clear value" then I'm curious how you would derive the clear category and the clear value? If one person says "I hate that house, I would only pay $300k for it" and another person says of the same house "I love that house, I would pay $600k for it" then who is correct?

If you want to have a sane conversation about this, I would suggest that you stop using the word "real." Use "inflation adjusted" if you mean that, and then use "actual" or "countable" when you mean those things.

About this:

"You keep confusing yourself by sometimes mushing the concepts inflation, asset price inflation, and consumer inflation and then getting upset when one doesn't fit neatly into the other."

I am not upset with you, nor did I say anything to suggest that I was upset with you. I'm simply pointing out that you don't seem to understand the words that you are using.

Also, I've avoided bringing politics into this, but it might be worth thinking of some of the notorious incidents of hyper-inflation, the political effects it had, and how such effects are simply not rational or possible or connected to increasing nominal prices for assets. I wrote about the late Soviet era hyper-inflation here:

There are different classes of assets but when I refer to real asset inflation it refers to real assets. I use real assets here since we are talking about houses. So to your question:

> If by "real" you mean "adjusted for inflation" then, again, you are double counting the inflation. If by "real" you mean "an object with a clear category and a clear value" then I'm curious how you would derive the clear category and the clear value?

I don't precisely mean either in regards to "real assets", see below.

>What is a real asset?

"Real assets are physical or tangible assets, such as infrastructure, real estate, natural resources and precious metals, whose value is based on their physical properties or utility." [0][1][2]

If I said "actual" or "countable" assets it would most definitely not have the same meaning. IOUs friend bill or a dollar bill are both actual and countable assets but not real assets.

>I would suggest that you stop using the word "real."

OK but to do so I'm going to need to see lkrubner's personal dictionary, since we are dispensing with the terms used in the financial industry.

>I hate that house, I would only pay $300k for it" and another person says of the same house "I love that house, I would pay $600k for it" then who is correct?

You can argue who is correct but when a house is for sale

the title is generally transferred to the highest bidder, all else equal. It really doesn't mean dick if I walk up to a house for sale and tell the owner I think it's worth $1000 bucks, nor does it mean anything if I think it's worth $1M and never pony up the money. When on a macro level we see the executed transaction for similar houses trend towards a price, it's safe to say the market roughly values houses similar to that house near that price.

>If by "real" you mean "adjusted for inflation" then, again, you are double counting the inflation.

Today I own one drill press as a capital for my manufacturing business. Tomorrow the .gov prints 1 quadrillion dollars. Tomorrow drill presses aren't any harder to come by nor harder to make nor any more or less useful for industry or for me or anyone else. The price inflation still rises. You can single, double, or triple or even fractionally count your idea of inflation in whatever made-up definition soup you want to conjure up, but the price inflation from more magic dollars entering circulation will still be there.

Interesting read. My take based on your writing is we should remove the money supply from the government, and instead decentralize as best we can to minimize the bad acts of a few actors. Widespread adoption of commodity money and privately issued notes (both fiat and asset backed) are a couple ways to reduce the influence of a single powerful government from having full control of the money supply.

"Today I own one drill press as a capital for my manufacturing business. Tomorrow the .gov prints 1 quadrillion dollars. Tomorrow drill presses aren't any harder to come by nor harder to make nor any more or less useful for industry or for me or anyone else. The price inflation still rises."

Future tense is compatible with a correct model, but present tense would be incorrect. No inflation has occurred even if the price goes from $100 to $100,000 for the exact same item. Again, as I've said several times elsewhere in this thread, when we are speaking jokingly or informally it is perfectly okay to say "asset price inflation" and everyone will informally understand what you mean. But I've been trying to explain how the government calculates inflation.

If the price goes from $100 to $100,000 for the exact same capital good that you own, you've become wealthier in nominal terms. However, you will need to pass along this price increase to those further down the line, either another company or a final consumer of some product of which your product might be a part. Once the final consumer sees the price increase, then the government will declare it to be inflation. But the government does not regard it as inflation in the CPI till it reaches the final consumer.

It might be a technical point, but it is worth keeping in mind: even those events that guarantee consumer inflation are not consumer inflation until they reach the final consumer. The distance in time might be weeks or years. Sometimes an event occurs and consumers feel the effect within a day -- gasoline prices are often like this, a terrorist attack in Saudi Arabia can see an uptick in prices within a day or two. Other times some event occurs and it takes years before consumers see the increase in prices; over fishing of the oceans is an event that almost guarantees consumer inflation, but typically takes several years to settle in, as the effect among the fish is multi-generational.

>But the government does not regard it as inflation in the CPI till it reaches the final consumer.

I think this really drills down into the crux of the problem that was posed. If you merely want to survive and not build up investments and capital for your later life and heirs, then consumer inflation gives you a good picture of how prices are raising around you and what your purchasing power looks like.

If you actually care about having some security for the future, land or assets for your business, preserving wealth for general use in any asset class, or something to pass on for your family, or being a PART of the world rather than just a consumer, then the CPI looks like a poor indicator of your changes in purchasing power.

The problem is these numbers get reported in headlines as “inflation”.

People are experiencing greater than 6% inflation in their pocketbooks. So I suppose I’m objecting to something different from what you’re talking about.

That is a valid issue that you raise, but unrelated to the conceptual issue of whether an increase in the nominal price of an asset can be coherently understood to be a form of "inflation." Hopefully everyone on Hacker News is smart enough to know that housing has special features that are different from other asset classes.

Define "housing". When it comes to shelter, that is taken into account.

> Anyone with a web browser knows that home prices have experienced a monumental increase.

Because the "C" in CPI stands for consumer. Home prices reflect asset prices. They are not counted in the CPI just like stock and bond prices are not counted: these are all asset classes.

> House prices are an interesting case. Houses are considered capital investment by the [US] BLS. So, when the value of your home increases that's a good thing as you didn't consume the house. In other words, you don't need to replace the house. Consumption goods are different in that you need to replace the thing you bought. Inflation is very bad for consumption goods because it costs you more to replace that thing each time you need it (food, for instance).

> The BLS views housing as a mostly “investment” item as opposed to a consumption item. So, for instance, when you consume a hot dog and have to replace it then the cost of replacement is a direct reflection on your well-being. A $1 hot dog that costs $2 one year later is a material change in living standards, all else equal, since the hot dog is an asset that you literally consume. A house is much more complex. [...]

>

> Of course, anyone who owns a house knows that it’s not that simple. You do basically consume your house over time. For instance, my home has appreciated substantially since I purchased it just 5 years ago and underwent a hellish remodel. At that time the cost of replacement was roughly $300 per square foot. But in the ensuing years the cost of replacement has increased to $400 per square foot. As my physical home falls apart over the years I will need to replace it. But the key point is that, as I replace these components the housing market is likely to revalue the total home value to account for this investment. So even though I am consuming my house over time I am very likely to recoup those costs.

Some company builds machines that make buttons. One of those machines lasts (say) 20 years. The machine is not buttons; the machine provides buttons. The company sort of provides buttons, but at one step removed.

We say that machine is an asset.

The machine is eventually "used up" over its lifetime, but that doesn't make it "consumable" in the sense used here - that's true of many assets (we call it "depreciation").

I think "house as button machine" is a consistent model that matches dragonwriter's usage.

> That's like saying homes don't provide shelter, construction companies do.

No, it's not. Food isn't a durable good that provides “nourishment” for consumption on an ongoing basis; agricultural real estate is, in exactly the same way as residential real estate is for shelter.

Housing prices have only gone up for people that have purchased a new house this year. For people already living in a house, mortgage payments have mostly been stable, or possible even lower, when refinancing for a lower rate. So i can imagine that the average housing costs have only gone up 3.8%.

I remember reading somewhere that only accounts for new contracts. Rents usually only increase when negotiating new leases or extending existing ones close to expiration. So the majority of renters are not paying that much more.

Mine in Seattle has not, even if I believe you in the general sense. I think my landlord valued having a renter with stable income from one of their former employers, so that might explain the lack of an increase.

And most people you know? It's exceedingly unusual for someone to drop rent. This is what rental/lease agreements stabilize. If you move or that there might be windfalls from some specific situations, is not the norm.

But houses are capital goods that generally appreciate in value, for the purposes of calculating CPI, treating them like consumption goods or like other consumer durables (e.g. vehicles) that generally depreciate seems odd to me.

the purpose of CPI, at least in my mind, is to calculate the change in the price of goods from year to year. Making your monthly mortgage payment isn't the same thing as buying a new house, so the fact that the payment might stay the same over the life of the mortgage contract doesn't seem particularly relevant. What seems relevant is how much it would cost to buy the same house again today.

For instance, if we suppose for the sake of example that the average American buys a new TV every five years, it would be true to say that the cost of TV for most Americans didn't rise this year even if TV prices increased 15%. But saying that seems to provide zero insight about CPI.

> Making your monthly mortgage payment isn't the same thing as buying a new house, so the fact that the payment might stay the same over the life of the mortgage contract doesn't seem particularly relevant.

In a thread about inflation, it's highly relevant. One of the biggest benefits to a mortgage is that you lock yourself into an inflation-resistant housing cost.

Lots of good replies here. One other thing to be conscious of is that inflation expectations play a large role in determining how actual inflation will pan out, so to raise the alarm on it in earnest is to the play a very dangerous game.

This is in part because they changed how CPI is calculated in the 80s and 90s, which, as luck would have it, lowered the rates. You can see what CPI looks like with the older formulas here to compare:

Shadowstats is one of the dumbest websites on the internet. It doesn't remotely compare to the older formulas, it just applies a random consistent number to US stats and says "They're undercounting!". If they really "recalculated" it wouldn't be a mirror of the official numbers.

Think about it logically, per their dumb chart, inflation has averaged ~10% since 2000? and something like 7% in the 1990s? That easily gets you to over 1,000% total inflation in the past 30 years. Are you paying 10x for anything compared to the 1990s? TVs? Computers? Food? Gas? Furniture? Cars?

The "C" in CPI stands from consumer, not assets. It is a measure of the cost of goods and services that people consume. Assets are not consumed so therefore not in the CPI.

> Also look at shrinkflation

Contrary to popular opinion, the people who calculate the CPI are not complete morons. See StatCan's (who do the CPI in Canada) handbook:

> 7.10 Quantity adjustment entails accounting for changes in the quantity (e.g. package size, number of tissue ply, etc.) of observed POs. This is another implicit method of quality adjustment because it is assumed that the quality per standardized unit is the same over time.

> 7.11 Quantity adjustment is the default treatment for nearly all of the POs in the food major aggregate as well as some of the products in the household operations, and personal care supplies and equipment aggregates.

Even in the most expensive cities in the US, rents are "only" up something like 250% in the past 30 years. And in most of the country, it's a small percentage of that.

Do you think that the economy has shrunk in half in real terms in the last 20 years? Because that’s essentially what it would mean for those numbers to be true.

Perhaps but even if that is the case, the general consensus appears to be that home purchase prices increased ~17 - 19% over the last year so right in line with the estimate by this site. If anything it would drag the estimate upwards.

OTOH, low interest rates have balanced that out, and let people who already have mortgages lower their monthly payment drastically. I wonder if monthly payment is perhaps a better metric than purchase price? At least for me, that's what actually determined how much home I'd be able to buy.

I also make trips to the store to buy proteins, maybe just not your kind of proteins. I usually get chickpeas, beans, edamame, lentils, etc) and I haven't noticed a change in price.

Soybeans are selling for $12.68/bushel today, compared to $11.53/bushel on December 10, 2020. So, yeah, they've gone up.

They have come down somewhat from their peak earlier in the year (though still significantly more than they were a year ago). In May they were over $16/bushel.

Lentils have just about doubled in price. $18.20/hundredweight in December '20, $36.20/hundredweight today.

The way inflation is measured is imperfect, but provides a consistent indicator. You may have more or less exposure to inflation which determines someone’s actual spending power

The Fed was initially saying the inflation was transitory, but have recently dropped the "transitory" label.

Back in July, Siegel pointed out that the M2 money supply is 30% over pre-pandemic levels and predicted that would translate into 20% cumulative inflation over the next 3 years. Here are my talk notes / video links if you're interested: https://neapowers.com/investing/jeremy-siegel/

In July Siegel said "There is zero need for the Fed to be buying $120 billion in bonds every month given market conditions." I don't know why the Fed is buying mortgage backed securities in the midst of an apparent housing bubble.

There's also an element here people don't talk: Covid created insane amounts of hard-to-repay debts. If interest rates go up quickly, the Govrermnent will suddently have to spend a lot of its budget on interest - expected, of course, but not something they are used to.

In NYC, many restaurants and property owners survived thanks to debt which will eat into their profits for years to come and may even bankrupt them down the road.

What is the answer to overwhelming debt? Inflation. Inflation makes the principle that you owe a lot cheaper and if you have borrowed in fixed interest rates, it makes the interest payments cheaper as well.

It would help both the government and the businesses mostly affected by Covid to run high inflation for a few years. This may or may not be part of the Fed calculation but I don't understand why nobody talks about it.

The poor have their week's worth of money that then gets taxed an extra 10-30%. The middle-class may sell some assets and be partly hit as a result. The wealthy will just hold their assets until the market settles down and lose nothing.

This is the exact opposite of a good economic solution.

The poor owe a fortune in debt to the wealthy, inflation wicks this away

As long as wages increase with, and they have to. If the poor can no longer as a whole afford to pay $1k in rent because the money goes on food, then they won't, and rental prices will have to come down because the demand for rental at $1k crashes (as nobody can afford it)

> This is the exact opposite of a good economic solution.

The system is built by and FOR the wealthy. The system is working exactly as designed: to hold down the middle and lower classes, giving them just enough to be happy but not enough to emerge from the rat race.

GDP per person in the US is around $50K. Some of the GDP has to go to investment and the government, so at best people can consume on average $30K worth of products/services per year.

Would you be happy consuming just $30K/year? I didn't think so.

The ratrace is not a matter of absolute numbers, it's because everyone wants to have more than their neighbors have and more than what their parents had. Also, everyone seems to want to spend 20% more than what they are making hence most people in the country are in (consumer) debt. Government is no exception and mirrors the behavior of the citizen.

This whole thing about the rich not giving enough money to the poor to keep them working is BS.

> It would help both the government and the businesses mostly affected by Covid to run high inflation for a few years.

The government is screwed if interest rates are high. They roll over their debt on an ongoing basis, and if interest rates go to even just ~5 percent then a huge chunk of the annual tax revenue will go to just repaying interest on the debt. The government (read: the people) cannot afford to have that happen unless drastic spending cuts accompany it. Recent events show that most legislators are interested in ramping up spending, not ramping down, which basically means that inflation would have serious consequences for the budget and economy.

I don't know if you were being rhetorical, but the Fed's motivation doesn't seem like that big of a mystery. They're succumbing to political pressure not to induce a recession or allow asset prices to drop.

As far as I can tell, the political class decided that no cost was too high to avoid being the one left standing when the music stops, after the '08 crash. So we'll just inflate until someone gets unlucky and is the one stuck with the blame for a massive crash rather than 2-3 smaller recessions inconveniencing some other politicians, who are actually the ones to blame for the whole situation. [EDIT] actually, arguably, the '08 crash was already an in-the-works recession delayed and made worse by exactly this kind of thing.

Another possibility is that someone realized something really awful, like that the global economy had shifted such that anything like the "asian contagion" crash (no, nothing to do with COVID[0]) can't be contained next time, so they're desperately trying to keep the plates spinning until they can figure something out, because they expect the next major crash will be a true global depression and don't know how to stop/mitigate it if it's triggered.

If the bubble pops, those securities are generally worthless. If I didn't know better, I'd say this is a move to bankrupt the US government. As it stands, it is idiocy and will bankrupt the government if things go sideways in the housing market.

Though, given the rate of inflation, the housing market may not pop as land is a secure asset that the wealthy are getting into.

They're buying those securities with printed money. It won't bankrupt the government, it will tank the dollar and everyone who has dollars, gets paid in dollars or loans dollars. Those borrowing dollars to buy assets and offload liabilities will be fine.

The first people getting those borrowed dollars (government contractors, banks selling treasuries and MBS, old people on social security) will be okay.

Since the dollar is an entirely Fiat currency, its supply is dictated purely at the whim of the U.S. Government.

This means that they can turn on the presses (or these days, make some keystrokes) and instantly have as much money as they want. Because of this, if there are outstanding debts that are denominated in USD, the government will always be able to have that money on hand, or create it.

The problem is that this puts more dollars out in the world. And if there are more dollars in circulation, everyone (on average) has a little bit more they can "bid" on consumer goods. Because of the law of supply and demand, things inflate in price.

The Federal Reserve is not the US Treasury. The Fed buys these mortgage-backed securities with money printed out of thin air. Likewise, the dollars disappear again as the mortgages mature. If the securities default, everyone who owns dollars bears the cost in the form of inflation, not the Fed.

It was obvious to anyone with an iota of critical thinking that it was not transitory. The way the government just printed billions of dollars was bound to result in inflation.

A lot of this is due to fuel prices. The price of fuel affects the price of everything else. It's a benchmark since everything requires fuel. Manufacturing, transportation, agriculture, etc. It all requires fuel. It doesn't help that OPEC refuses to increase production in order to make up for their budget shortfalls last year. Also doesn't help that the US government is sending signals that it is no longer on board with fossil fuels. The shutting down of pipelines, ending of fossil fuel leasing, etc. sends a market signal to producers and traders that the US is hostile towards the industry, leading the producers to cut production and maintain their profits.

Best option would be to have a diverse portfolio of energy production: oil, natural gas, solar, wind, hydroelectric, and nuclear. Don't go all in on one, that's how you arrive at the situation we are currently in.

> sends a market signal to producers and traders that the US is hostile towards the industry, leading the producers to cut production and maintain their profits.

Great! Puts us one step closer to slowing global warming and giving us a chance to turn this boat around.

Rising oil prices makes the market naturally move away, which is really really good in the long run.

That will disproportionately affect lower income households who can't as easily withstand these rising costs, which further drives income inequality.

> Rising oil prices makes the market naturally move away

This is trivialization of the transition as the worlds depends oil in many ways: development of cars (electric or otherwise), airplanes, solar panels, vaccines, acetaminophen, etc. -- these are all petroleum-derived products.

Given this dependence, axing our production just means we have to rely more on other countries and given that climate change is a global problem -- what's the difference? If we do it here, perhaps we innovate on making its extraction more eco friendly (which has been the case for the last 20 years)

> That will disproportionately affect lower income households who can't as easily withstand these rising costs, which further drives income inequality.

I see your compassion, but income inequality isn't driven by prices, it's driven by the employers not paying enough to their employees. Prices can't fix that.

> This is trivialization of the transition

Is it? I read it more as this being an important step toward addressing the climate crisis.

> as the worlds depends oil in many ways

How much oil is used in making acetaminophen? Why even bring it up? Nobody is saying "no oil," they're saying "stop polluting so much".

> perhaps we innovate on making its extraction more eco friendly

The extraction is a small problem. The global warming it causes is the large problem. Less pumped oil means less burned oil which means fewer greenhouse gases.

> I see your compassion, but income inequality isn't driven by prices, it's driven by the employers not paying enough to their employees.

Not exactly, it's also driven by price increases. If employers give their employees a 50% pay increase, but prices increase by 50% then that pay raise is rolled back by inflation. Wealthier people more often have their money in assets, with values that increase alongside inflation. This is largely the dynamic we're seeing in the US: labor shortage means people get paid more, but those increased wages are getting eaten by higher prices.

Very low income people frequently have more debt than assets. They also see their net worth increase from inflation.

Also the sources I see show nominal wages growing faster than inflation for low income households, meaning that their real wages are actually increasing.

> I see your compassion, but income inequality isn't driven by prices, it's driven by the employers not paying enough to their employees. Prices can't fix that.

The two are intertwined. Every big-ticket item costs at least $1000 round numbers these days. If you halved that threshold to $500, you would put more valuable goods in reach to more people without adjusting wages.

You can do the same by increasing wages, but that threshold might go up in response to $2000.

It’s all about prices relative to wages, not either in isolation

this is why focusing on the wage part of inequality is the wrong approach.

Figure out how to make products cost less and cheaper -> more can enjoy them and everyone becomes richer.

Print more money to give to people to fight inequality? If you don't invest to make supply more efficient, all you'll get is inflation.

Rich people don't buy the same products as poor people. In fact, most rich people (Elon) own capital that is being invested in part to make production more efficient.

If you were to tax all of Elon's wealth and give it to the poor, it's just not the case that everyone could suddenly afford a Tesla. What would happen is that nobody could afford it, even people that can afford it today, because you are moving capital away from investment and into consumption.

it does, but you also have to tax some people so that they spend less.

Recent narratives is that you can do welfare for 'free', either by printing money and not worry about inflation or default, or by taxing 'billionaires' so nobody feels it except 100 people.

Climate change will also disproportionately lower income households.

> perhaps we innovate on making its extraction more eco friendly

Wait what? Fossil fuels will never be eco friendly. The best thing for renewable energy is to be more economical than their competitors, which is far more achievable when oil is expensive. It should be obvious that oil prices doubling do not cause electric cars or solar panels to double in price, even if they do become slightly more expensive.

Well that's just false. As of 2020 US reduced its emissions by over 20% below 2005 levels which was mostly due to fracking natural gas instead of coal.

Not saying that's all rainbows either but you're suggesting there can't possibly be any improvement here. Sounds like a bad bet.

You claimed that the best way to make oil consumption more eco friendly was by reducing the environmental impact of extracting it, rather than letting high cost motivate consumers to switch to renewables. Now you've backtracked to supporting natural gas to replace coal. It is true that switching from coal to natural gas is a big win for CO2 emissions, but there are clear diminishing returns on that. Since 2005, the US has already gone from 50% coal power to 20%. The problem is that our current levels of oil and natural gas consumption are incompatible with hitting emissions targets. The mere act of burning those fuels at the current rate already puts those targets out of reach -- before even considering the cost of extracting them.

> The shutting down of pipelines, ending of fossil fuel leasing, etc. sends a market signal to producers and traders that the US is hostile towards the industry, leading the producers to cut production and maintain their profits.

That's the point isn't it? From an environmentalist perspective, policy that discourages fossil fuel production makes renewables more economically attractive by comparison, encouraging attrition away from fossil fuels into renewables, thus reducing emissions.

> Best option would be to have a diverse portfolio of energy production: oil, natural gas, solar, wind, hydroelectric, and nuclear.

Pretty much everyone can agree with this statement, the devil is in the details as usual.

Interesting, I thought the US was now "energy independent" but Forbes is claiming we're now short.

> However, thus far the price surge is primarily a result of 3 million barrels per day (BPD) of oil production that was lost in the spring of 2020 that hasn’t fully recovered. Demand has fully recovered, so that is the fundamental reason for the surge in prices. Further, that surge began in the fall of 2020 — five months before President Trump left office.

The shutdown hit oil production quite a bit. Recovery and startup lag by months.

All the Democrat candidates put themselves forward as anti-oil. If you thought Trump would lose, it would be smart to buy oil and then hold for a while.

When Biden won, the speculation took off. Signals matter.

Biden signaled that everyone must move away from gas-driven vehicles. He banned a pipeline (getting sued by Canada over that one). He banned as much fracking as he could. Even worse, he defied congress and the law by allowing the Russians to build their pipeline which will pipe money straight into Putin's pocket

The result of these changes (and others) was a lot of people shutting down oil production. Others speculated even more that the pipeline and fracking decrease would mean less supply, so they bought up the oil while the prices were still down.

With OPEC refusing to up production, there's even less reason for the speculators to sell. Biden released part of the strategic reserve, but it amounted to less than two days supply of oil for the country and nobody who knew anything about the oil market cared very much.

Crude prices have been a lot higher in the past, 2007-2008. The production is fairly in line with the demand.

US actually needs higher crude prices to make sure the incentives exist for shale production to get back to pre covid levels.

The supply chain sluggishness (worldwide) combined with excessive, irresponsible spending (although I hear it "costs nothing"...) explain these figures.

Euro area has higher inflation than pre covid but nowhere near these levels.

It's becoming increasingly clear that the "it's transitory" narrative is dead wrong. But now all the policy makers are committed to the lie. I fear this will make any reaction much slower and weaker than it otherwise might be. Are we going back to the stagflation of the 70's? How should one prepare financially for that possibility?

You could ask your employer to match the inflation with a raise every year (on top of the actual raises you might've earned). I think this is a reasonable ask, though understandably not all companies are able to cover the inflation by raising their prices etc.

When it comes to protecting your assets from inflation, I suppose investing in companies that pay good dividends and are able to cover the inflation in their business model should be a relatively safe bet, as they continue to provide a steady cashflow. If you think the inflation is here to stay and you want to take on more risk, you could take out a loan and leverage that by investing it, as the inflation should cover the interest.

Note that this is NOT financial advice -- I'm anyway not qualified to give that, so take this only as food for thought.

If the value of the dollar is at risk then preparing financially means getting out of the dollar by getting some assets that are not priced in dollars or physical assets that have intrinsic value.

I am leaning more heavily on physical assets as even foreign stocks will suffer to some extent in the event of a dollar crisis. With USD as the current global reserve it's failure will ripple through financial markets and economies around the world.

The best thing you can do is learn how these kinds of things have played out in the past and make a plan to "weather the storm" as it were. I have really been enjoying stories of living through high inflation in other countries on https://www.youtube.com/c/StarPathAcademy. Not saying that is where we are certainly headed but all of the indicators are the same as other high/hyper-inflation periods in history.